PROFESSIONAL AND PERSONAL GUIDANCE

When bringing a company to the Netherlands to start a new endeavor, Dutch fiscal policies are important factors. A solid combination of the corporation tax rates in the Netherlands and financial incentives, make the country a reliable choice as a base for international operations. The Dutch Tax Authorities have a flexible and practical approach, with a proactive attitude.

PRACTICE AREAS

Competition by the numbers

Corporate income tax rates in the Netherlands are currently 16.5% for the first €200,000 of taxable profits and 25% for taxable profits exceeding €200,000. A special optional tax rate may be elected for profit resulting from (patented) intangible assets, by placing these in a special tariff box on your corporate income tax return: the innovation box.

Among other benefits related to the Netherlands tax policy, consider the following:

- A wide network of nearly 100 bilateral tax treaties to avoid double taxation and to provide, in many cases, reduced or no withholding tax on dividends, interest and royalties.

- Clarity and certainty in advance on the tax consequences of proposed major investments in the Netherlands.

- A broad participation exemption (100% exemption for qualifying dividends and capital gains), which is vital for European headquarters.

- An efficient fiscal unity regime, providing tax consolidation for Dutch activities within a corporate group.

- No statutory withholding tax on outgoing interest and royalty payments.

- For companies looking to bring employees from abroad, the 30% ruling allows employers to offer 30% of employee salaries tax-free in order to compensate for the extra costs costs international employees incur when moving to the Netherlands.

Stimulating innovation and sustainable foreign investment and entrepreneurship

The Netherlands actively supports new ideas and innovations. By creating a nurturing fiscal environment for forward-thinking companies, the Netherlands stays competitive on the world stage and supports innovation and sustainable investments:

- R&D tax credit, or WBSO: offers startups and innovative companies compensation for part of the research and development (R&D) wage costs, other costs, and expenditures.

- Energy Investment Allowance (EIA): allows companies to deduct 45% of the investment cost of energy-saving equipment from the taxable profit in addition to the deduction of the customary depreciation.

- Environmental Investment Deduction (MIA): allows companies to deduct up to 36% of the investment costs for an environmentally friendly investment on top of the regular investment tax deductions

- Arbitrary depreciation of environmental investments (Vamil): allows companies to amortize 75% of the investment costs of a qualifying environmentally friendly investment at once.

Besides the above incentives, companies can also chose to apply for a Innovation Credit: a credit for companies with innovative ideas.

VAT Deferment

Although VAT is highly integrated in the EU, the member states have some discretion in certain areas. Some advantages of the Dutch VAT regime:

- VAT deferment upon importation: no actual payment of VAT

- Experience with the international trade in products

- Experienced and specialized Tax and Customs officers

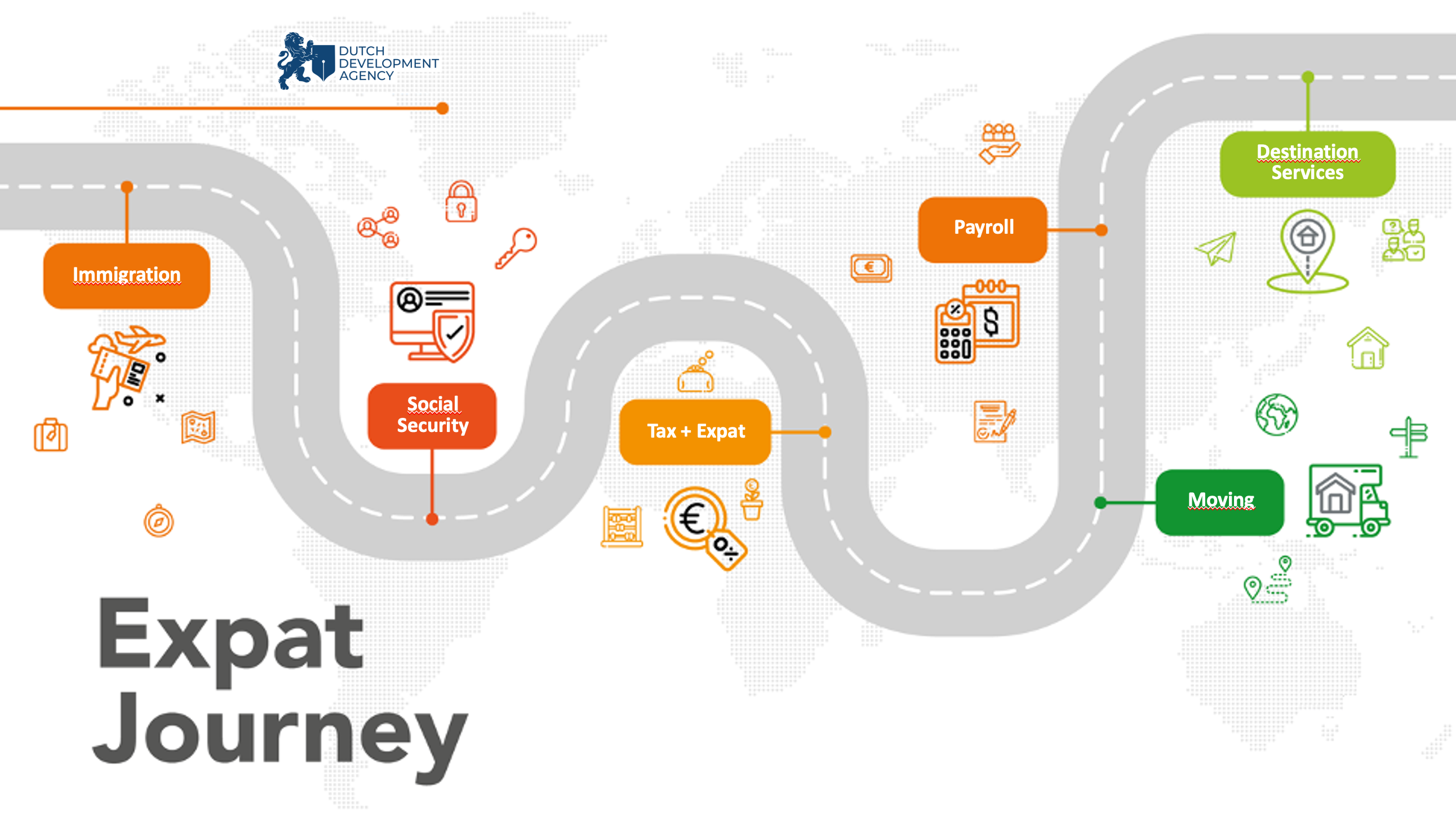

EXPAT JOURNEY

Dutch Development Agency (DDA) helps and advises foreign companies in the various stages of establishing, rolling out and expanding their international activities in the Netherlands